Read more

13 October 2023

Safe, secure & confidential

“Can I get a mortgage while in a Consumer Proposal?” It’s one of the most common questions people ask after they’ve taken steps to deal with unsecured debt. And fair enough. Sorting your finances out does not magically switch off life plans like buying a house, refinancing, or renewing your mortgage.

The short answer is this: yes, it can be possible to get a mortgage while in a Consumer Proposal in Canada, but it depends heavily on the lender type, your down payment, your income stability, and your overall risk profile.

As our Licensed Insolvency Trustees have noticed, Consumer Proposals consistently account for the vast majority of formal insolvency filings compared to bankruptcies. That matters because lenders see this scenario often. They have policies for it. Some are rigid. Some are pragmatic. None are sentimental.

Key Points

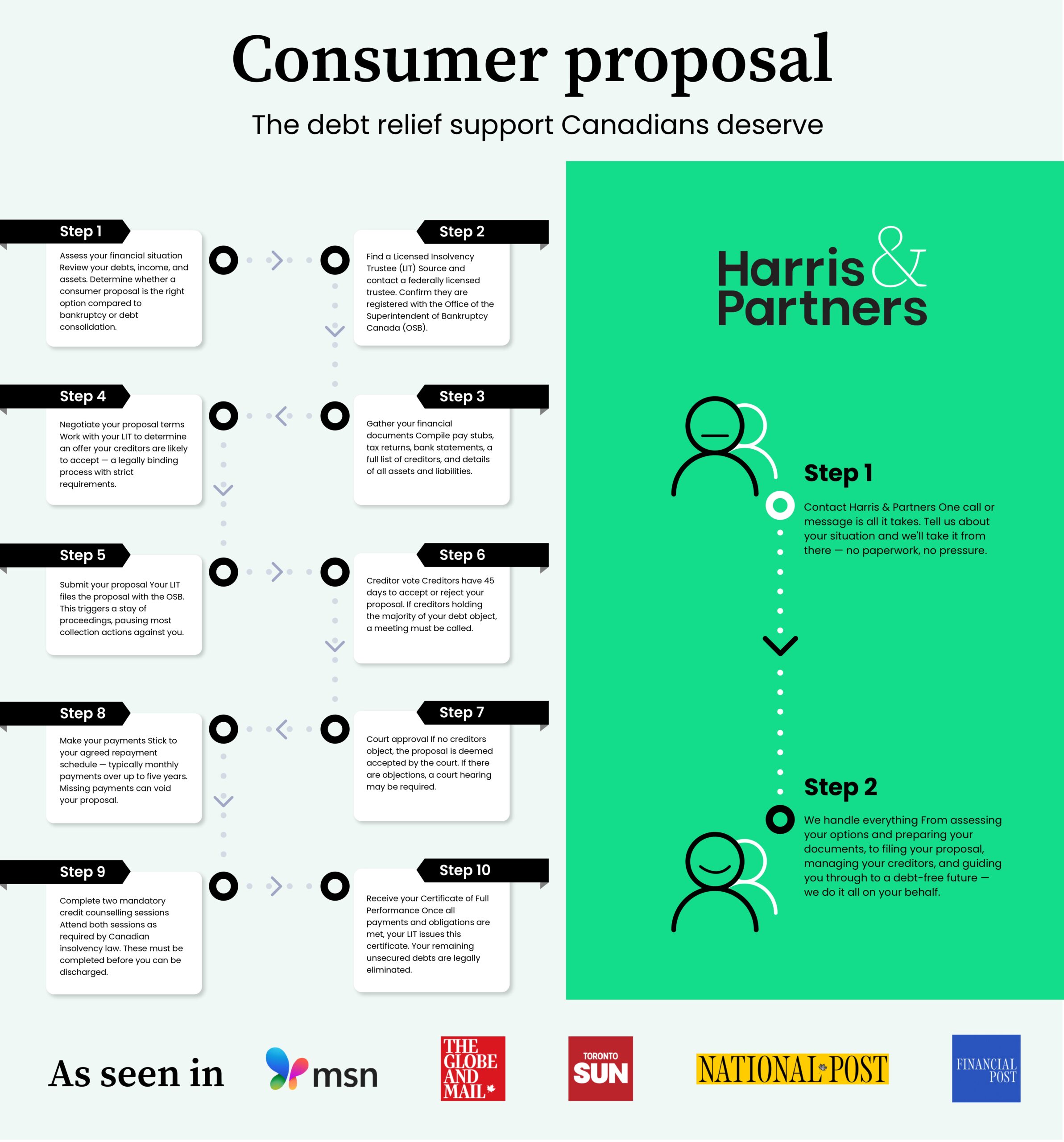

A Consumer Proposal in Canada is a legally binding agreement filed under the Bankruptcy and Insolvency Act that allows you to settle unsecured debts through one affordable monthly payment over a set period (often up to five years), instead of trying to keep up with multiple creditors.

Only a Licensed Insolvency Trustee (LIT) can file and administer a Consumer Proposal in Canada, under the supervision of the Office of the Superintendent of Bankruptcy (OSB).

When it comes to Consumer Proposals, one important thing to note is:

This means your existing mortgage is not automatically rewritten, reduced, or eliminated through a Consumer Proposal. If you continue making your mortgage payments, you usually keep your home.

From a lender’s perspective, however, a Consumer Proposal is recorded on your credit report and often associated with an R7 credit rating. That’s where the friction begins.

Lenders care about Consumer Proposals because it implies risks. They signal that:

For a prime lender—such as a bank or credit union—this is a major underwriting event. For an alternative lender—like P2P platforms—it is a risk factor that can sometimes be canceled out by equity, down payment size, and a strong income.

This is why the question is not just:

“Can I get a mortgage while in a consumer proposal?”

but:

“Which lender would consider me, at what rate, and under what conditions?”

If you already have a mortgage and you continue making Consumer Proposals payments on time, most lenders will not immediately interfere.

Important distinctions include:

However, if you fall behind on your mortgage while in a Consumer Proposal, the situation escalates quickly. Secured lenders retain their enforcement rights.

So in simple terms:

This is where people get caught off guard. When your mortgage term ends, you face:

If you renew with the same lender and your payment history has been clean, approval may be smoother because they already hold the security. If you try to switch to a new prime lender during an active consumer proposal, you are effectively applying for new credit. That often triggers stricter underwriting scrutiny.

So if you are asking:

“Will a consumer proposal affect my mortgage renewal?”

The honest answer is:

It depends on whether you stay with your current lender and how strong your file looks.

A Consumer Proposal can make refinancing your mortgage more difficult. Refinancing is not passive. It is a new credit decision. When you refinance, you are asking a lender to:

Alternative or private mortgage lenders may consider it, especially where there is:

But it often comes with:

This is where “mortgage while in a consumer proposal” becomes a math problem, not a moral one.

Yes, you can sometimes get a mortgage during a consumer proposal. But it depends almost entirely on lender category.

Prime lenders focus heavily on:

An active Consumer Proposal is usually a barrier. Some may consider applications after completion and seasoning (a period of clean credit rebuilding), but during the Proposal, prime approval is uncommon.

That does not mean impossible in every scenario, but it is rarely straightforward.

Alternative lenders operate with more flexibility.

They often consider:

You may hear repeated advice that a 20 percent down payment is needed. That’s because:

Rates are typically higher than prime rates, but approval may be realistic under the right structure.

Private lenders are asset-driven.They focus primarily on:

They are less focused on credit score, but are also significantly more expensive. Private mortgages are often short-term solutions, not long-term homes for your financing.

Used strategically, they can bridge you from active Consumer Proposal to post-completion refinance with a stronger lender. Used poorly, they become a high-cost trap.

If you are researching “Can I get a mortgage while in a Consumer Proposal”, you will often see 20% mentioned. That’s not random.

A 20 percent down payment:

In many active Consumer Proposal cases, this threshold is the difference between “no” and “maybe”.

If your downpayment is under 20%, your mortgage may require default mortgage insurance. When you are in a Consumer Proposal:

This is why high-ratio mortgage approvals during an active Consumer Proposal are significantly more challenging. In practice, many borrowers either:

Our first-party data shows that Consumer Proposals represent the dominant share of formal insolvency proceedings compared to bankruptcies.

That means:

So while a Consumer Proposal affects your mortgage options, it does not automatically disqualify you from ever owning property. It shifts you into a different lane of lending.

Getting a mortgage approval during or a Consumer Proposal is possible in some cases, but heavily dependent on lender type, down payment, and risk profile.

Let’s take a look at:

This is where “mortgage after Consumer Proposal” becomes a timeline and preparation exercise rather than a yes-or-no question.

You can get a mortgage after a completing a Consumer Proposal as you are no longer in an active insolvency proceeding. That changes how lenders assess risk.

There is no single rule for how long after a Consumer Proposal you can get a mortgage. However, patterns across underwriting policies typically include:

For prime lenders, a seasoning period is often required. For alternative lenders, approval may be possible sooner, especially with a strong down payment. The longer the time since completion, the stronger your mortgage approval chances generally become.

A Consumer Proposal drops off your credit report some time after completion. While the exact duration depends on reporting agency rules, it does not stay forever. Lenders care less about the historical event itself and more about:

The key concept here is credit rehabilitation. Time plus clean behaviour equals lower perceived risk.

You can get a mortgage sooner after your Consumer Proposal is done. Some borrowers do not want to wait years. In those cases, the pathway often involves:

This is where “exit strategy refinance” becomes critical. If you go this route, you must understand:

Used strategically, it accelerates homeownership. Used impulsively, it locks you into expensive borrowing.

From down payment to affordability, lenders look at a few major factors when approving your mortgage after a Consumer Proposal:

What size down payment can you provide?

Down payment strength is one of the biggest compensating factors. In many Consumer Proposal mortgage scenarios, lenders expect:

Because higher equity lowers the loan-to-value ratio (LTV) and reduces lender exposure.

Do you pass affordability standards?

Even if you have completed your proposal, you still need to qualify under affordability standards. Lenders assess:

If your housing costs plus other obligations exceed policy limits, approval becomes difficult regardless of your insolvency history. A Consumer Proposal does not remove the math from the equation.

Do you have stable income and employment?

Lenders want predictability. They prefer:

If you combine unstable income with a recent insolvency event, risk compounds quickly.

Have you re-established your credit?

This is non-negotiable for prime lenders. After a Consumer Proposal, rebuilding credit usually involves:

Over time, this strengthens your mortgage application file.

Step-by-step: How to improve your mortgage approval chances during a Consumer ProposalIf you are serious about getting a mortgage while in a Consumer Proposal, or soon after completing one, here’s what you can do—step by step.

Before thinking about buying property:

In our first-party data, Consumer Proposals represent the majority of formal insolvency filings. That volume means lenders are experienced at spotting unstable financial behaviour. Consistency is your strongest signal.

Do not open five accounts hoping for a miracle.

Instead:

Credit rebuilding is about pattern formation, not speed.

If you are asking, “Can I get a mortgage during a consumer proposal?”, the most practical lever is equity.

A larger down payment:

Not every mortgage broker has access to alternative lenders experienced in insolvency files.

You may need:

A well-structured file can mean the difference between rejection and conditional approval.

Here are some real-world situations that you may find yourself in that may be affected by being in a Consumer Proposal.

Here are some things to avoid when it comes to mortgages while in a Consumer Proposal:

A Consumer Proposal is a financial reset tool. Turning it into a springboard for new unsustainable debt defeats the purpose.

Can you buy a house while in a consumer proposal in Canada?

Yes, it’s possible to buy a house in Canada while you’re in a Consumer Proposal, but most buyers use alternative (B-lender) or private lenders rather than prime banks. You’ll typically need a larger down payment (often 20% or more), stable income, and a clean recent payment history to be considered.

Will a Consumer Proposal affect my mortgage renewal?

A Consumer Proposal can affect your mortgage renewal. If you’re renewing with your current lender and you’ve kept mortgage payments up to date, it is often more straightforward than switching lenders during an active Consumer Proposal. If you need to change lenders at renewal, expect tighter approval rules, more documentation, and potentially higher rates.

How long after a consumer proposal can I get a mortgage?

The time it takes to get a mortgage after a Consumer Proposal depends on the lender. Many prime lenders prefer the Proposal to be completed and for you to show a period of re-established credit afterwards. Alternative lenders may consider you sooner, especially if you have a strong down payment, stable employment, and improving credit behaviour since filing.

Can I refinance my mortgage while in a consumer proposal?

Refinancing during a Consumer Proposal is more likely if you have significant equity and strong affordability. However, it can involve higher interest rates, stricter underwriting, and fewer lender choices than a standard refinance.

Do I need 20 percent down to get a mortgage after a consumer proposal?

You don’t need it, but having 20% down often improves your approval chances and can make the application process simpler. With a smaller down payment, you may face additional restrictions, fewer lender options, and stricter qualification requirements.

A mortgage while you’re in a Consumer Proposal can be realistic—but only with the right expectations and the right plan. At Harris & Partners, our Licensed Insolvency Trustees will review your situation, explain what lenders are likely to accept right now, and help you understand what you can do next to move forward with confidence.

Book your free consultation now or call us on 800–268–8093 for a private, no-pressure conversation focused on what you can realistically manage, and the quickest, cleanest route to homeownership.

Partner, Licensed Insolvency Trustee at Harris & Partners Inc.

Joshua Harris is a Licensed Insolvency Trustee and Partner at Harris & Partners Inc. With a strong background in financial restructuring, Joshua has been instrumental...

Read more

Read more

Read more

Read more

Read more

Read more

Read more

Read more

Read more

Read more