Read more

12 October 2023

Safe, secure & confidential

Almost half of all Canadians find themselves with less than $200 to spare by the end of the month, leaving them vulnerable to financial challenges. In today’s uncertain economic climate, unexpected expenses can easily push you into debt, leaving you uncertain about your next steps.

You might be burdened by debt, but you could also have valuable assets you wish to protect. Concerns about the long-term repercussions of bankruptcy may be on your mind. Fortunately, there’s an alternative solution – a Consumer Proposal, which can offer you a fresh financial start.

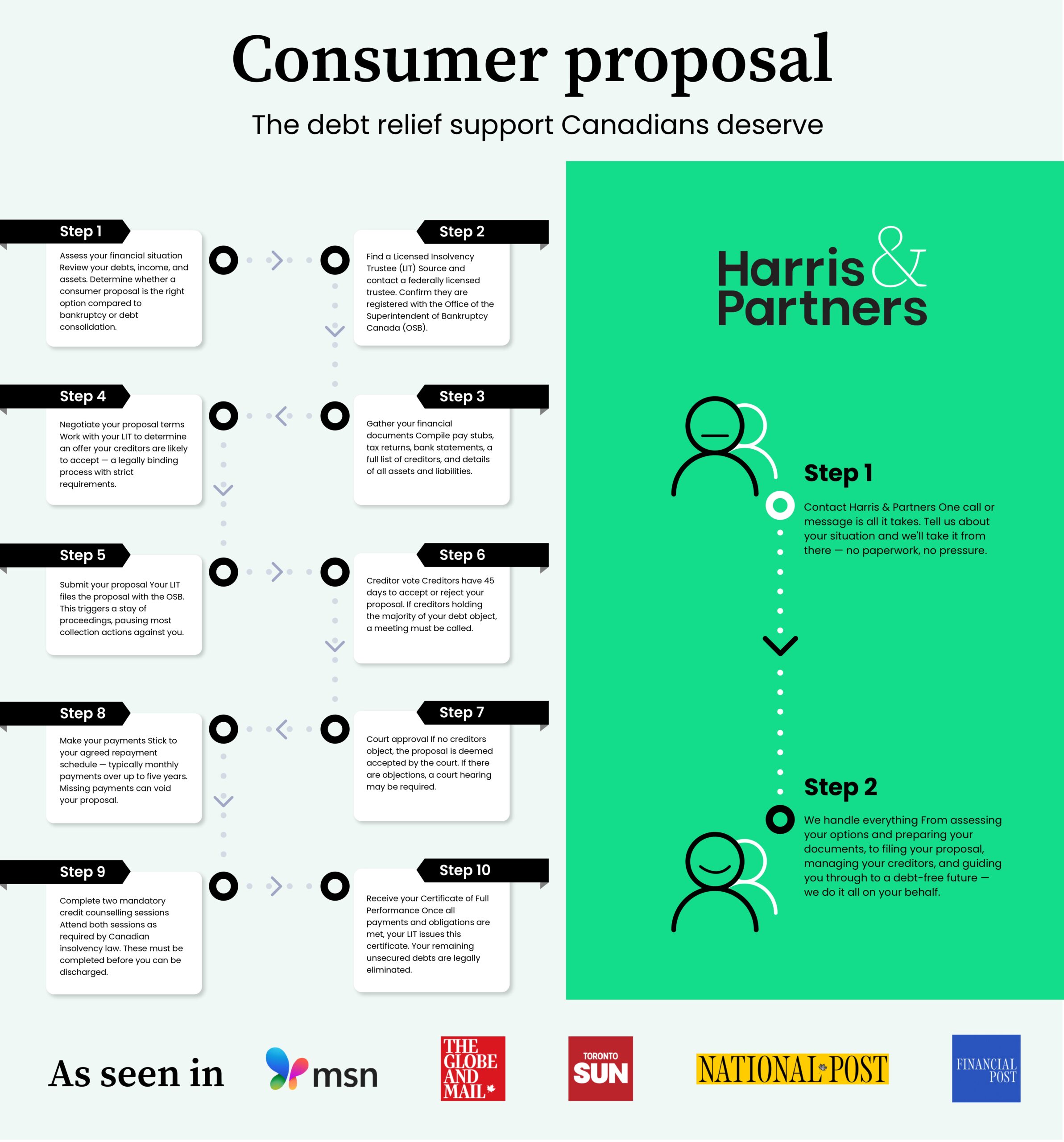

If you’re grappling with financial stress and struggling with payments, seeking guidance from a Licensed Insolvency Trustee at Harris & Partners is a wise step. They can help you explore options and propose a debt repayment plan to your creditors. Harris & Partners provides expert assistance and complimentary debt counseling to assist you in regaining financial control.

Now, let’s assess the advantages and disadvantages of filing a Consumer Proposal to help you determine if it’s the right solution for your unique circumstances.

Key Points

Consumer proposals can provide significant benefits in managing overwhelming debt, making them worth considering. Here are key reasons to explore a consumer proposal:

Consider these factors to decide whether a consumer proposal is the right solution for your debt challenges. Consulting a Licensed Insolvency Trustee is a vital step in making an informed decision.

If your debt is starting to feel overwhelming, a consumer proposal might be the help you’ve been looking for. They offered a structured way for you to regain financial control, stopping your debt from snowballing with fees and penalties and pooling all your debts into one manageable, monthly payment.

Other benefits of a consumer proposal include:

Throughout the Consumer Proposal process, you’ll benefit from the knowledge and support of a Licensed Insolvency Trustee (LIT). The LIT communicates with your creditors on your behalf and guides you through every step.

Before choosing a consumer proposal, it is important to have the full picture. As with any debt help solution in Canada, consumer proposals come with some disadvantages. These are:

Not sure if a consumer proposal is right for you? Get in touch with one of our Licensed Insolvency Trustees today – they can talk you through the details and help you find the best debt solution for you.

Dealing with debt is never simple, but the good news is you don’t have to face it alone. With our help you can find your path to financial independence – we’re here to support you every step of the way.

If you want to chat about consumer proposals in Canada, get in touch today.

Partner, Licensed Insolvency Trustee at Harris & Partners Inc.

Joshua Harris is a Licensed Insolvency Trustee and Partner at Harris & Partners Inc. With a strong background in financial restructuring, Joshua has been instrumental...

Read more

Read more

Read more

Read more

Read more

Read more

Read more

Read more

Read more

Read more